The global two-wheeler hierarchy has undergone a rare shift in CY2025, with TVS Motor Company overtaking Yamaha to become the third-largest manufacturer by volume, marking a milestone for India’s auto industry. But the achievement also underscores a deeper structural gap: Collectively, Indian manufacturers continue to trail their Japanese rivals by over 10 million units annually.

Honda alone sells more than 20 million units globally, while Yamaha and Suzuki together outpace the combined volumes of India’s ‘Big Three’ — Hero MotoCorp, TVS Motor, and Bajaj Auto. For TVS, the more immediate challenge lies closer home, where it trails Hero and Honda in the domestic market.

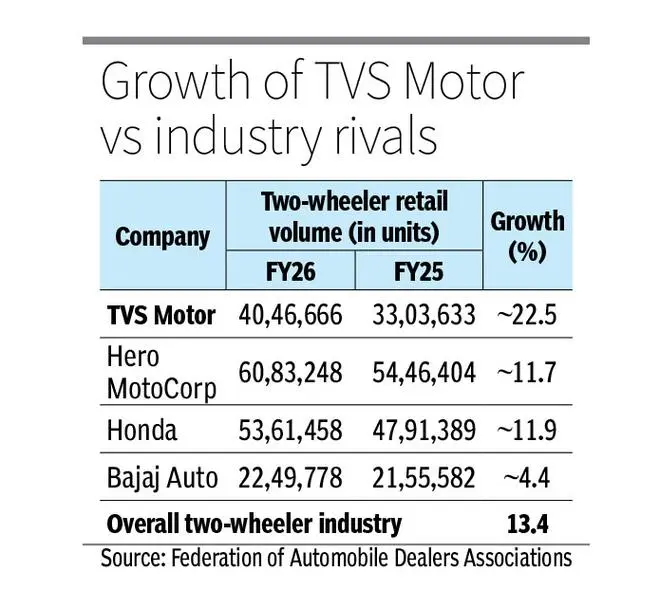

Closing the gap

The gap, however, is narrowing.

TVS Motor’s rise has been driven by a strategy anchored in outpacing industry growth. “We are confident that we will do better than the industry growth, both in domestic and international markets,” Managing Director KN Radhakrishnan said during a recent earnings call.

This outperformance is already visible in retail trends. According to Federation of Automobile Dealers Associations (FADA) data for FY26, TVS grew its retail volumes by 22.49 per cent, way beyond the industry’s 13.4 per cent growth.

KN Radhakrishnan, Managing Director, TVS Motor Company

Its market share rose to 18.89 per cent from 17.49 per cent a year earlier, while Hero MotoCorp’s share edged down to 28.4 per cent. The shift is even more visible against Honda — the gap between Honda Motorcycle and Scooter India and TVS narrowed to 6.14 percentage points in FY26 from 7.88 percentage points a year earlier.

Premiumisation

At the core of this momentum is a calibrated shift toward premiumisation. The company has leaned into feature-rich motorcycles and scooters such as the Raider, Apache range, Jupiter, and Ntorq.

“Premium and super-premium are growing faster,” Radhakrishnan said. This shift is being validated — and increasingly seen as structural, rather than cyclical.

“Growth is being driven by a richer domestic vehicle mix and higher export volumes,” Axis Securities said in a recent sector note, pointing to improving realisations and stronger product positioning.

Kotak Institutional Equities, in its March quarter earnings preview, endorsed this view and expects this shifting mix to continue driving earnings improvement.

Together, these assessments suggest that TVS Motor’s growth is not merely volume-led but increasingly also quality-led — better pricing, stronger mix, and a widening presence in higher-margin segments.

The strategy is also portfolio-led. “We always look at the total portfolio contribution… we don’t look segment-wise,” Radhakrishnan said.

A changing demand cycle

This positioning is reshaping the domestic market. TVS is capturing urban demand through premium products while riding a rural recovery. FADA data shows rural growth at 13.05 per cent and urban growth at 13.62 per cent in FY26, pointing to a convergence that increasingly favours higher-spec models.

The traditional divide between rural and urban consumption is narrowing, expanding the addressable market for premium offerings.

“With the kind of infrastructure getting built in India… mobility needs… and affordability, I’m a firm believer that 8–9 per cent CAGR is sustainable,” Radhakrishnan said.

Exports power growth

International markets are emerging as a key growth engine. TVS has expanded across Africa and Latin America. “The demand in Africa continues to grow… LatAm also has grown,” Radhakrishnan said.

Analysts see exports as both a volume and margin lever. “A higher export mix is supporting margins across auto companies,” Kotak noted, linking international expansion to improved earnings quality.

Yet Southeast Asia remains the toughest market. Indonesia and Vietnam continue to favour Japanese incumbents, making ASEAN the last frontier for Indian OEMs.

The EV wild-card

Electric mobility could reset the competitive order, but also determine whether TVS can translate momentum into leadership.

TVS emerged as the market leader in India’s electric two-wheeler segment in FY26, retailing about 341,513 units and capturing a 24 per cent market share, according to FADA data.

The 43.5 per cent year-on-year growth helped it overtake early mover Ola Electric.

Unlike several competitors, TVS has taken a calibrated approach — scaling up through its iQube platform while leveraging its distribution network and brand strength. This has helped it expand beyond early adopters to more mainstream buyers — a shift that has proved challenging for both start-ups and legacy players.

EV penetration is also rising. FADA data shows electric two-wheelers accounted for 6.54 per cent of total volumes in FY26, with monthly penetration nearing double digits.

This positions EVs not just as a new segment but also a structural shift that could reshape market share over time, potentially accelerating TVS Motor’s climb in the domestic hierarchy.

Legacy strengths

However, the transition comes with trade-offs. “Margins could be impacted by the margin-dilutive mix of EV scooters,” Axis Securities said, highlighting near-term profitability pressures.

At the same time, Kotak noted that “operating leverage and improved product mix” continue to support margins, suggesting that legacy strengths remain relevant even as EV investments rise.

For TVS, the EV strategy mirrors its broader approach. “Continue to grow the top line… improve the product mix,” Radhakrishnan said.

The challenge will be in converting early leadership into durable scale as the market shifts from subsidy-driven adoption to demand-led growth.

The road ahead

At the premium end, TVS is sharpening its global ambitions through Norton Motorcycles. “We will have a differentiated strategy for Norton,” Radhakrishnan said.

The rise to the global top three marks a coming-of-age moment, but not the endgame.

Closing the gap with Hero at home will test its ability to scale up. Cracking ASEAN will test its global ambition. And making EVs profitable will test its execution discipline.

The climb to third was about momentum. The climb to second will be about execution.

More Like This

Kamal Sharma, Nilesh, Vinita, Desh Bandhu Gupta")

Published on April 13, 2026