istock.com/scyther5

| Photo Credit:

scyther5

Banks have knocked on the Reserve Bank of India’s door, seeking relaxation to spread the provisioning they will need to make for the losses incurred by their bond portfolio due to substantial hardening of yields in the fourth quarter (Q4) of FY26.

Their ask is that the provisioning for mark-to-market losses on investments should be allowed to be spread over four quarters beginning Q4FY26. This will take the pressure off their bottomline.

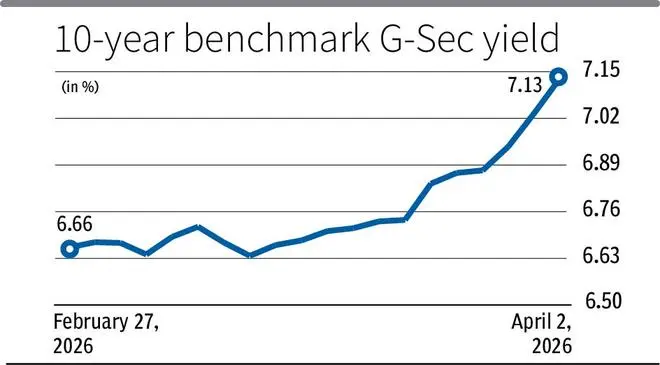

Spike in G-Sec yields

In the fourth quarter (Q4FY26: January-March), Government securities’ (G-Secs) yields spiked, especially from February-end, with the onset of the West Asia war.

For example, yield of the 10-year benchmark G-Sec (6.48 per cent GS 2035) jumped 45 basis points (bps) to close at 7.04 per cent on March 30, 2026 (last day of trading in Q4FY26) against the December-end 2025 closing level of 6.59 per cent.

The last time banks had made a similar request to RBI was in 2018, and the regulator had allowed banks to spread their losses (due to sharp increase in G-Sec yields) by providing for depreciation on investments over four quarters, commencing from the quarter in which the loss was incurred.

Bond yields and prices are inversely co-related and move in opposite directions. So, with the yield of the aforementioned G-Sec rising 45 bps, its price crashed about ₹3 in the fourth quarter.

The war has triggered concerns in the bond market that rising global crude oil prices could have an inflationary effect in the economy. This, in turn, may require the RBI’s rate setting panel (the monetary policy committee) to up the repo rate in either its June or August monetary policy review to curb inflationary pressures.

Treasury portfolio hit

Bankers say it is not just banks that have taken a hit on their treasury portfolio, but the RBI too could face the heat of spike in G-Sec yields. They pointed out that the central bank purchased G-Secs aggregating about ₹7 lakh crore from banks under its open market operations (OMOs) to provide them durable liquidity in FY26.

“So, the central bank’s portfolio of G-Secs purchased under the OMO window too will be subject to the impact of spike in yields. This could have implications for declaration of dividend to the government for FY26,” said a banker.

The RBI transferred ₹2,68,590 crore as surplus to the Central government for FY25. The Union Budget for FY27 has budgeted a dividend/ surplus of ₹3.16 lakh crore from Reserve Bank of India, nationalised banks and financial institutions against ₹3,04,590 crore (revised) for FY25.

Venkatakrishnan Srinivasan, Founder & Managing Partner, Rockfort Fincap LLP, said that while rising yields typically result in mark-to-market pressures on bond portfolios, banks — being natural participants in the bond market— may have largely managed this risk through active portfolio rebalancing and prudent treasury management.

“As a result, treasury losses are likely to have been contained to an extent. At the same time, with strong double-digit credit growth, improved net interest margins, and significantly lower NPAs, the overall profitability of banks in the last fiscal year is expected to remain robust. This provides some cushion to the system, even as bond market volatility persists,” he said.

Published on April 5, 2026