A proposal within the Securities and Exchange Board of India (SEBI) to raise the upper age limit for managing directors (MDs) and chief executives of market infrastructure institutions (MIIs), to be more aligned with the corporate sector, has met with resistance from industry participants, according to people familiar with the discussions.

The proposal suggested increasing the current age cap from 65 to 70 years for top executives at MIIs, including stock exchanges such as the National Stock Exchange of India (NSE), BSE Ltd , Metropolitan Stock Exchange of India (MSE), commodity exchanges like National Commodity and Derivatives Exchange (NCDEX) and Multi Commodity Exchange of India (MCX), as well as the two depositories and clearing houses.

Sources said the proposal is currently at a discussion stage, with SEBI seeking industry feedback before moving forward with public consultation. Most peers are understood to have opposed the move, questioning its broader rationale.

The discussions have also exposed divisions within SEBI, with two distinct views among officials, a source said.

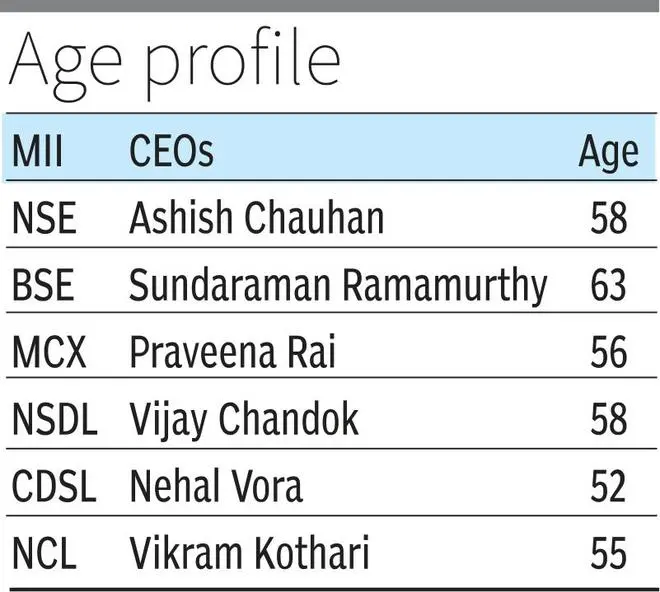

The proposal comes at a time when Sundararaman Ramamurthy, managing director and chief executive of BSE, is among the incumbent MII heads approaching the current age threshold of 65. The tenure of Arun Raste, Managing Director & Chief Executive Officer of National Commodity & Derivatives Exchange, ends this June.

“The current limit ensures timely transition and avoids overdependence on individuals. This discipline should not be diluted for at best one immediate beneficiary,” a source said.

Industry pushback

Relaxing the age cap is expected to weaken succession planning and institutional renewal.

“Extending the age limit could delay leadership transitions and affect the pipeline for next-generation executives,” said a senior exchange official. “In a country of India’s scale, it is difficult to argue that capable leadership options are scarce. Fresh perspectives are increasingly valuable, especially as markets become more technology-driven.”

Another source said, “These are not ordinary companies. They operate critical market infrastructure. Stability is important, but so is periodic refresh in leadership.”

Regulatory framework

At present, SEBI regulations for MIIs prescribe both tenure limits and an upper age cap of 65 for MDs and CEOs. While executives can typically serve fixed terms, often up to five years per appointment, subject to board and regulatory approval, the age limit acts as a hard stop.

These norms are part of a governance framework tightened over the past decade to address concerns around ownership, control, and conflicts of interest at systemically important market institutions.

MIIs are subject to stricter fit-and-proper norms and governance standards, as they are treated as public utilities given their central role in price discovery, clearing and settlement, and overall market stability.

Any move to revise the age cap would require SEBI board approval and public consultation. An email sent to SEBI seeking comments did not elicit a response.

Published on April 26, 2026