By Ruth Carson, Masaki Kondo and Winnie Hsu

Japan’s investors are starting to lose their decades-long infatuation with overseas assets.

Click here to connect with us on WhatsApp

In the first eight months of the year, Japanese investors snapped up a net ¥28 trillion ($192 billion) of the nation’s government bonds, the largest amount for the time frame in at least 14 years. They also cut purchases of foreign bonds by almost half to just ¥7.7 trillion and their buying of overseas equities was less than ¥1 trillion.

“It’s going to be one of the mega trends and it is a super cycle for the next five to 10 years,” said Arif Husain, head of fixed-income at T. Rowe Price, who has nearly three decades of investing experience. “There will be a sustained, gradual but massive flow of capital back into Japan from abroad.”

With $4.4 trillion invested abroad, an amount larger than India’s economy, the speed and size of any pullback has the power to disrupt global markets. Even as the gap in rates between Japan and other countries has narrowed, the inflows have been a trickle rather than the flood some investors have feared.

The overseas investments of the Japanese have been compared to a giant carry trade, where investors benefited from ultra-low interest rates available at home to fund purchases abroad.

The scope of the flows will depend on the pace and trajectory of rates in Japan. While Bank of Japan Governor Kazuo Ueda indicated policymakers would be more measured on plans to hike, strategists are almost unanimously forecasting a stronger Japanese currency into next year on views policy will inevitably normalize.

Yields on the benchmark 30-year Japanese government bonds have risen about 40 basis points to above 2% as the BOJ has raised rates this year. That’s getting closer to the point where some of the country’s biggest insurers intend to amp up their holdings of local debt.

T&D Asset Management Co. has said a 30-year JGB yield above 2.5% can be a level where money flows back home. Dai-ichi Life Insurance Co. said in April that yields above 2% on these bonds would be relatively attractive. The yen weakened 0.4% to 144.16 to the dollar on Wednesday.

Japan Post Insurance Co. is still investing offshore, but “it has become easier to invest in yen-denominated assets,” said Masahide Komatsu, senior general manager at the firm’s global credit investment department. “We want to diversify our investments.”

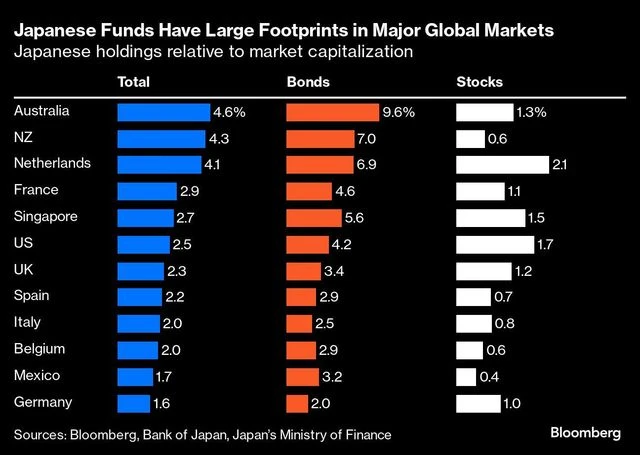

The stakes are massive: Japan’s investors are the largest foreign holders of US government bonds and own almost 10% of Australia’s debt. They also control hundreds of billions of dollars worth of stocks from Singapore to the Netherlands and the US, owning anywhere between 1% and 2% of the markets. Their reach extends to high risk investments such as cryptocurrencies and risky debt that blew up in Europe.

They built up holdings during the years of sub-zero rates at home and snapped up everything from Brazilian bonds that yield over 10% to Alphabet Inc. shares and bundles of risky loans in the US.

One prominent example of the drive to go overseas is Norinchukin, Japan’s largest agricultural bank, which invested a significant chunk of its ¥60 trillion securities portfolio in US and European government debt. It is now in the process of unwinding about ¥10 trillion in foreign holdings after an unexpected spike in rates increased its funding costs and saddled the bank with losses. San-in Godo Bank Ltd., a regional bank based in western Japan, also plans to bulk up its holdings of JGBs while selling off Treasuries.

A nightmare scenario for markets would be an even more extreme version of the chaos of Aug. 5, when fears of higher Japanese rates and a slowing US economy led to a rapid unwinding of carry trade bets by global hedge funds and other overseas speculators. The Nikkei 225 suffered its biggest rout since 1987, Wall Street’s stock volatility gauge spiked, and the yen advanced. Even gold, a haven in time of stress, fell.

Japanese investors — including some of the world’s biggest pension funds and insurers — largely laid dormant, underscoring the potential for more tectonic shifts.

The turmoil also prompted the BOJ to say it would take market conditions into account before raising rates again and would hold off if markets were unstable. Additionally, the Federal Reserve cut rates by half a percentage point in September, in an effort to preserve the strength of the US economy.

“August gave us a glimpse into the repatriation trend,” said Charu Chanana, a global markets strategist at Saxo Markets. “The Fed’s commitment to achieving a soft landing has reduced the odds of a recession. This means future repatriation may not be as abrupt.”

While policy is normalizing, Japan’s rates remain hundreds of basis points below counterparts like the US and Europe, meaning offshore assets still appeal to yield-hungry investors willing to tolerate currency risk. Japan’s Government Pension Investment Fund, one of the world’s largest pension funds, targets about half of its holdings in foreign bonds and equities. Those positions helped it offset losses in domestic debt during its last reporting period.

Japanese investors are “realizing that the US markets are still incredibly liquid, very large, offer the most diversification,” said Anders Persson, global head of fixed income at Nuveen LLC. “They’re looking for a little bit more yieldy-type opportunities.”

After the market chaos in August, JPMorgan Chase & Co. estimated that as much as three quarters of the carry trade had been unwound. That analysis looked at global trades funded by borrowing in currencies with low rates. With a BOJ benchmark rate of 0.25%, the yen still fits that criteria. As that changes, the incentives for the Japanese to bring their money home will grow.

“Investors everywhere are underestimating the risk of big repatriation flows in the long run,” said Shoki Omori, chief desk strategist at Mizuho Securities Co. in Tokyo. “The Japanese are big carry traders themselves. The trend is already underway — watch this space.”

(Updates with yen in 8th paragraph)

"Chart")

"Chart")

"chart")

"chart")