Electric four-wheelers (E4Ws) saw a boost in in May 2026 driven by sharply rising fuel prices, a wave of new model launches and improving consumer confidence in electric mobility.

Registrations of E4Ws rose 82 per cent year-on-year in May 2026 to 25,509 units from 14,006 units in the same month last year, according to Vahan data collated as at 9 am on June 1. On a month-on-month basis, registrations increased 14 per cent from 22,405 units in April.

As per Crisil estimates, EV penetration as share of total passenger vehicle registrations has moved steadily higher, from 4.9 per cent in March 2026 to 6.4% the following month and to 6.9 per cent in May 2026.

Industry experts said the surge reflects a combination of economic and market factors. The steep increase in petrol and diesel prices during May widened the running-cost advantage of electric vehicles, while a growing range of products across segments, particularly SUVs, attracted a broader set of buyers. The entry of new manufacturers and continuous product launches have also expanded consumer choice and boosted market visibility

Since March 2026, monthly registrations have averaged around 25,000 units, compared to roughly 17,300 units through most of FY26, a jump of close to 45 per cent, pointing to a meaningful shift, said Poonam Upadhyay, Director, Crisil Ratings. Fuel costs have been a key factor. Petrol and diesel prices rose by a cumulative ₹7.50 per litre across four revisions in May 2026 alone, and with global crude supply remaining uncertain, direction of fuel prices is unlikely to ease in the near term, she said.

The recent hikes have widened running cost advantage of EVs further, and buyers in cities with reasonable charging infrastructure are increasingly factoring that in. OEMs expanding into the mid-SUV segment have also brought more buyers into the consideration set. The combination of sharply higher fuel costs and wider product choice is driving sustained uptick in monthly volumes, she added.

Gaurav Vangaal of S&P Global Mobility says that a meaningful part of India’s E4W volume expansion can be attributed to the growing cadence of new launches continuously adding incremental units to the segment. Each new model entry brings its own buyer cohort, and collectively these additions are stacking up into visible growth, he said.

“The segment’s long-term health will depend on whether these incremental launches are seeding a loyal, repeat buyer base — or simply redistributing the same early-adopter pool across a wider set of nameplates,” he said.

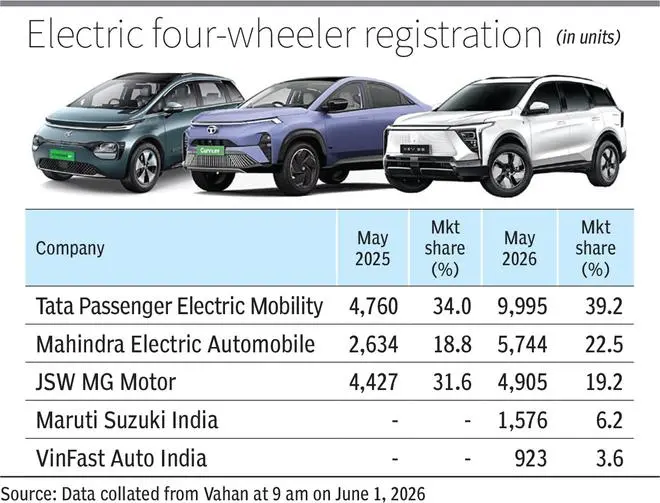

Tata Passenger Electric Mobility retained its leadership position in the electric car segment, while Mahindra Electric Automobile emerged as the fastest-growing major player in the segment. Tata recorded 9,995 units during May. The company more than doubled its sales from 4,760 units in the corresponding month last year, registering a growth of nearly 110 per cent. Its market share grew to 39.18 per cent from 33.99 per cent a year ago and from 37.09 per cent in April 2026.

Mahindra recorded sales of 5,744 units in May 2026, representing a growth of 118 per cent. Its market share improved to 22.52 per cent from 18.81 per cent a year earlier, although it was marginally lower than the 23.09 per cent recorded in April.

JSW MG Motor sold 4,905 units during the month, up 10.8 per cent from 4,427 units in May 2025. Despite the increase in volumes, its market share declined significantly to 19.23 per cent from 31.61 per cent a year ago, indicating stronger growth by rivals.

Maruti Suzuki India, a recent entrant to the electric passenger vehicle market, sold 1,576 units in May, accounting for a 6.18 per cent market share. The company had sold 1,222 units in April, when its share stood at 5.45 per cent.

Vietnamese electric vehicle maker VinFast Auto India also continued to gain traction in the market. The company registered sales of 923 units in May, compared with 831 units in April, giving it a market share of 3.62 per cent, says the data.

Published on June 1, 2026